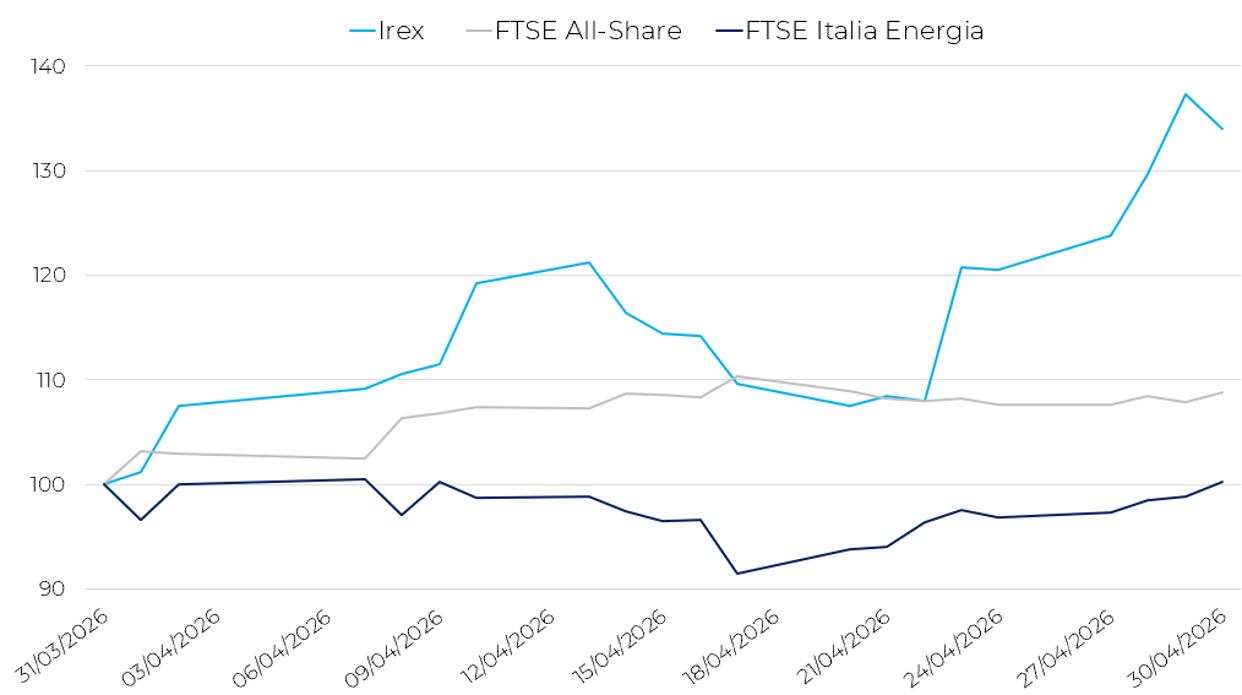

After the strong recovery recorded in March, the Irex Index continued its positive trend and closed April sharply higher. The basket of Italian small- and mid-cap companies active in the renewable energy and smart energy sectors reached 31,510 points, marking a 34% increase compared with the end of March. Monthly performance was particularly volatile, with an initial phase of rapid acceleration, followed by intermediate corrections and a renewed strengthening during the second half of the month. The result reflects continued speculative interest in the sector, supported by technical short-covering and renewed risk appetite for highly volatile stocks.

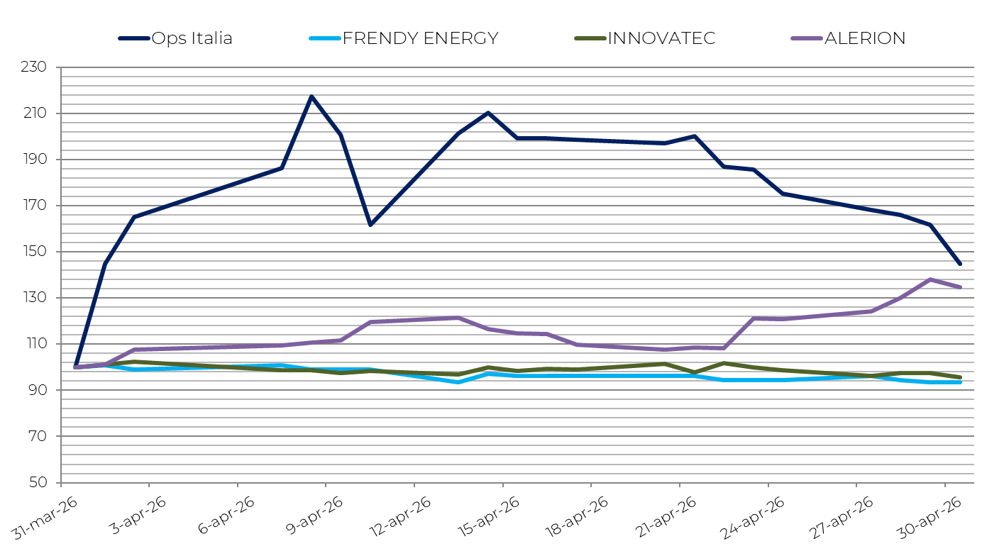

The overall picture shows a significant improvement, driven mainly by stocks that had experienced the steepest corrections in previous months. EEMS (+44.9%) led the basket’s recovery, benefiting from high volatility and speculative buying. Alerion (+34.6%) also posted a strong performance, confirming its recovery trend, supported by positive quarterly results. The only companies to remain in negative territory were Frendy Energy (-6.5%) and Innovatec (-4.2%): the former was affected by declining hydroelectric production data, while the latter suffered from uncertainty surrounding its strategic management following its negative 2025 result.

The Irex Index significantly outperformed the main Italian stock market indices. In April, the FTSE Italia All-Share rose by 8.9%, reflecting a broad improvement in stock market sentiment, while the FTSE Italia Energia remained substantially stable (+0.3%), delivering a considerably weaker performance. This trend highlights a strong relative recovery of the renewable energy sector compared with traditional energy stocks, following the severe oil market shock that began the previous month.

Major European stock indices also returned to positive territory in April. Germany’s DAX gained 7.16%, while France’s CAC 40 increased by 3.74%. Spain also posted a positive performance, with the IBEX 35 rising 3.94%. Overall, European markets benefited from a partial improvement in investor confidence, supported by a moderate easing of geopolitical tensions and reduced pressure on energy prices compared with the peaks reached in March.

In the energy commodities market, April showed signs of partial normalization, although developments differed between Brent and WTI crude oil following the sharp price surge of the previous month. Brent fell to $113.84 per barrel, down 4.1% from March, while WTI rose moderately to $105.46 per barrel (+3.95%).

In the Italian electricity market, the PUN (Single National Price) declined to €119.47/MWh, down 16.69% compared with March. This evolution reflects less strained supply conditions and a partial reduction in energy risk premiums, although prices remain elevated by historical standards.

The international macroeconomic environment remains fragile and heavily influenced by geopolitical tensions. According to the OECD, global growth is expected to reach 2.9% in 2026 and 3.0% in 2027. The conflict in the Middle East has further increased risks in energy markets, pushing oil prices higher and driving significant increases in gas prices across Europe and Asia. In Italy, the latest ISTAT data point to a mixed picture: in March 2026, industrial production increased by 0.7% compared with February and by 1.5% year-on-year, suggesting a moderate strengthening of industrial activity. Meanwhile, inflation accelerated to +2.8% year-on-year in April (+1.2% month-on-month), driven mainly by energy prices. Consumer confidence declined to 90.8 from 92.6 the previous month, indicating greater caution among households.

Overall, April highlights a strong increase in the Irex Index, supported by the rebound of renewable energy small- and mid-cap companies following the period of stress observed during the first quarter. However, volatility remains high, driven both by the geopolitical environment and by developments in the energy market. While awaiting further regulatory and macroeconomic developments, investors continue to focus on the financial strength of the companies included in the basket and on their ability to benefit structurally from the energy transition.

Worst e best performers