After the strong recovery recorded in April, the Irex Index interrupted its positive trend and closed May with a sharp decline. The basket of Italian small- and mid-cap companies active in the renewable energy and smart energy sectors stood at 28,055 points, marking an 11% decrease compared with the end of April. Monthly performance was highly uncertain, featuring an initial recovery during the middle part of the month, followed by a sharp correction starting in the third week and further weakening toward month-end. The performance reflects renewed pressure on higher-volatility stocks, in a context where the renewable energy sector continues to display significant sensitivity to sector rotation and profit-taking following the strong rebound of the previous month.

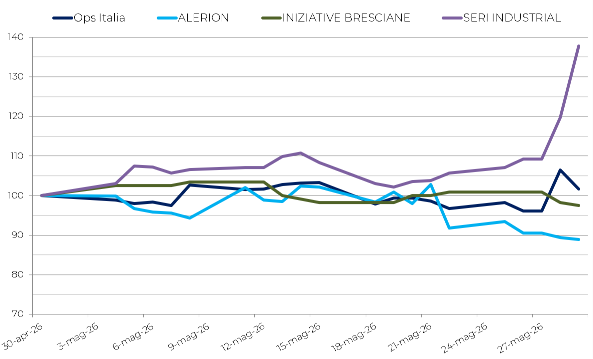

The performance of individual stocks was mixed, with a strong rise in SERI Industrial contrasting with the weakness of the basket’s main constituents. SERI Industrial (+37.7%) clearly led the monthly rankings, benefiting from the announcement of an agreement between Eni Industrial Evolution and FIB, a SERI Group company, aimed at developing an integrated industrial supply chain for lithium iron phosphate batteries. The deal strengthened market interest in the stock, thanks to its growth prospects in energy storage systems for both stationary applications and electric mobility. Innovatec (+1.6%) and Ecosuntek (+1.2%) also recorded positive, albeit much more modest, gains, while EEMS and ESI ended the month broadly unchanged. On the downside were Frendy Energy (-2.0%), Iniziative Bresciane (-2.6%), and especially Alerion (-11.1%), which weighed significantly on the overall performance of the index. Alerion’s decline appears mainly attributable to technical and financial factors, including the dividend distribution and the launch of its capital increase.

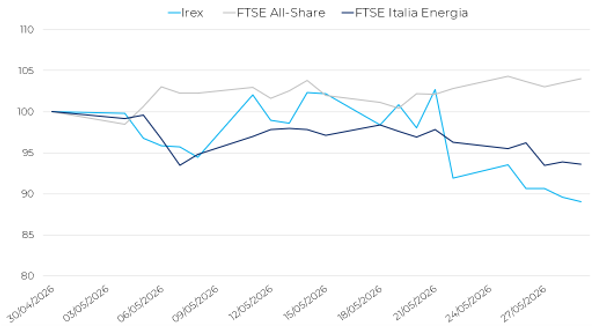

The Irex Index significantly underperformed the main Italian stock market indices. In May, the FTSE Italia All-Share gained 4%, confirming improved sentiment in the domestic equity market. By contrast, the FTSE Italia Energia fell by 6.4%, reflecting weakness in traditional energy stocks and the correction in oil prices. This trend highlights a double divergence: on one hand, the Irex Index markedly underperformed the broader Italian market; on the other, the renewable energy sector experienced a deeper correction, signalling increased risk aversion toward the sector’s small- and mid-cap stocks.

Major European stock indices also closed the month in positive territory. Germany’s DAX rose by 3.5%, while France’s CAC 40 gained 0.8%. Spain’s market also performed well, with the IBEX 35 advancing 3.3%. Overall, European markets benefited from a more favorable confidence environment compared with previous months, although they remained influenced by geopolitical uncertainty and expectations regarding future monetary policy decisions. Comparison with European benchmarks confirms the relative weakness of the Irex Index, which failed to benefit from the broad recovery across major equity markets during the month.

In energy commodities markets, May saw a sharp correction in oil prices. Brent crude fell to $92 per barrel, down 19.2% from April, while WTI declined to $88.1 per barrel, a decrease of 16.4%. This development reflects a partial reduction in the risk premium embedded in crude oil prices following the tensions of previous months, although the market remains exposed to developments in the Middle East conflict. In the Italian electricity market, the PUN (Single National Price) remained substantially unchanged at €119.4/MWh, virtually stable (-0.1%) compared with April.

The international macroeconomic environment remains fragile and heavily influenced by developments in the Middle East conflict. The OECD notes that disruptions to shipping through the Strait of Hormuz and damage to energy infrastructure have once again put pressure on the global economy, contributing to higher prices for energy, fertilizers, and other critical industrial inputs. Under the scenario of limited disruption, global growth is expected to slow from 3.4% in 2025 to 2.8% in 2026, before recovering to 3.1% in 2027. Inflation across G20 countries is projected to rise to 4.0% in 2026 before easing to 3.1% in 2027 as pressures on energy and food prices gradually subside.

For Italy, the outlook remains weak. The OECD forecasts GDP growth of 0.5% in 2026 and 0.6% in 2027, constrained by higher energy prices and persistent uncertainty, while harmonized inflation is expected to reach 3.0% in 2026 before falling to 2.2% in 2027. The report also highlights a particular vulnerability of the Italian economy, which is more exposed than other major euro-area countries to supplies of refined petroleum products and natural gas passing through the Strait of Hormuz, accounting for approximately one-quarter and 11% of total supply, respectively.

Overall, May was characterized by a sharp correction in the Irex Index, weighed down by renewed pressure on highly volatile stocks. As investors await further corporate, regulatory, and macroeconomic developments, attention remains focused on the financial strength of the companies in the basket, their ability to generate industrial growth, and the resilience of the energy market in an environment still marked by considerable uncertainty.

Worst e best performers