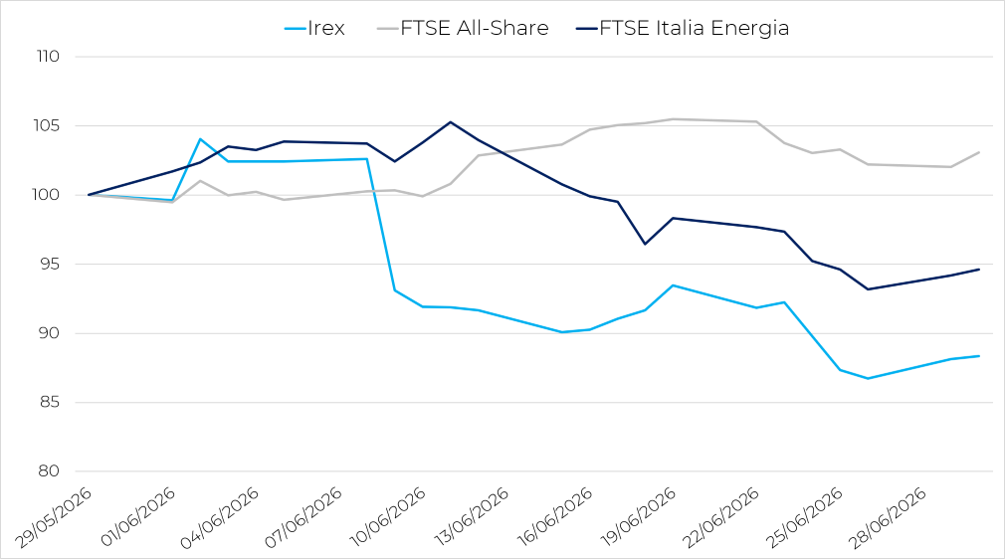

Following the correction recorded in May, the Irex Index extended its negative trend and closed June with a further decline. The basket of Italian small- and mid-cap companies active in the renewable energy and smart energy sectors stood at 24,784 points, down 11.7% compared with the end of May. After a relatively stable first week, the index experienced a sharp correction during the second half of the month, followed by a final phase characterized by high volatility, although without a sufficient recovery to return to early-month levels. The performance reflects a renewed climate of caution toward the renewable energy sector, weighed down by increasing geopolitical uncertainty and a rotation of investments toward sectors perceived as more defensive.

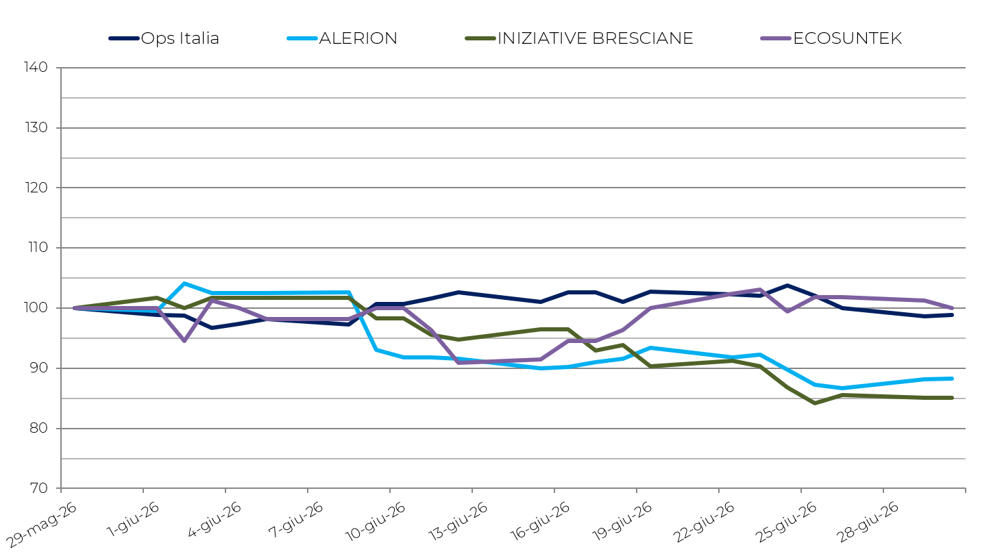

The performance of individual stocks confirms an overall difficult month for the basket. Innovatec (+5.1%) was the best-performing stock of the month, supported by a technical rebound following weakness observed in previous months. At the opposite end, Fri-El Green Power (-5.1%) and ESI (-5.8%) posted moderate declines, while SERI Industrial (-11.7%) and EEMS (-11.7%) recorded steeper losses, reflecting the persistent volatility typical of smaller-cap stocks. The weakest performances came from Iniziative Bresciane (-14.9%) and, above all, Alerion (-17.7%). The former continued to suffer from the weakness already highlighted in its 2025 results, marked by a sharp drop in profits and a reduced dividend, within a context of limited liquidity that tends to amplify market movements. Alerion, on the other hand, was affected by technical pressure related to the capital increase completed during the month, with newly issued shares offered at a discount to market prices, as well as by investors’ growing focus on the group’s financial leverage.

As a result, the Irex Index significantly underperformed the main Italian equity benchmarks. In June, the FTSE Italia All-Share gained 3.07%, confirming an overall positive environment for the domestic equity market, while the FTSE Italia Energia declined 5.40%, reflecting lower oil prices and increased volatility within the energy sector. The trend highlights how renewable energy small- and mid-cap stocks experienced a much deeper correction than both the broader Italian market and the traditional energy sector.

Major European stock indices showed mixed performances during June. Germany’s DAX declined by 0.50%, while France’s CAC 40 rose 2.70%. Spain delivered the strongest performance, with the IBEX 35 advancing 5.98%, supported in particular by banking and industrial stocks. Overall, European markets continued to demonstrate resilience, although they remained heavily influenced by geopolitical uncertainty and expectations regarding future monetary policy decisions.

In energy commodities markets, June was marked by a significant correction in oil prices. Brent crude fell to $73.0 per barrel, down 20.59% compared with May, while WTI crude declined to $70.3 per barrel, a decrease of 20.24%. This trend reflects the reduction of the risk premium embedded in crude oil prices following tensions recorded in the previous month, although the international environment remains exposed to developments in the Middle East conflict. In the Italian electricity market, however, the PUN (Single National Price) increased to €132.50/MWh, up 11.02% compared with May, reflecting market conditions that remain tight and highly volatile.

The conflict in the Middle East remained the main source of risk for the global economic outlook. Tensions in the Strait of Hormuz and damage to energy infrastructure pushed up the prices of energy, fertilizers, and other industrial inputs, affecting inflation, confidence, and economic activity. Under its baseline scenario, the OECD expects global growth to slow from 3.4% in 2025 to 2.8% in 2026, before recovering to 3.1% in 2027. G20 inflation is projected to rise to 4.0% in 2026, from 3.4% in 2025, before easing to 3.1% in 2027. However, the outlook remains highly dependent on the duration of the energy shock. Should disruptions persist through 2027, the OECD estimates global growth would weaken substantially to 2.1% in 2026 and 1.8% in 2027, with additional pressures on prices, interest rates, financial markets, and investment activity. The euro area would also remain fragile: under the baseline scenario, growth is expected at 0.8% in 2026 and 1.2% in 2027, while global trade growth would slow from 5.0% in 2025 to 3.1% in 2026 and 2.9% in 2027.

For Italy, the latest ISTAT data continue to depict a weak economic environment. According to preliminary estimates, in June 2026 inflation (NIC, excluding tobacco) showed no monthly change and increased by 3.0% year-on-year, slightly slowing from 3.2% in May. Core inflation also eased marginally to 1.6%, from 1.7% in the previous month. Consumer confidence declined from 93.4 to 92.4, reflecting a deterioration in households’ assessments of the economic environment, while business confidence improved from 94.2 to 95.2, supported by gains across manufacturing, construction, services, and retail trade.

Overall, June marked a further weakening of the Irex Index, which continued to underperform the main Italian and European equity markets. Rising geopolitical uncertainty, persistent volatility in energy markets, and increased risk aversion toward small- and mid-cap stocks all contributed to deepening the sector’s correction. While awaiting further macroeconomic, regulatory, and corporate developments, investors remain focused on the financial strength of the companies within the basket, the evolution of the international energy landscape, and the sector’s ability to benefit from policies supporting the energy transition.

Worst e best performers