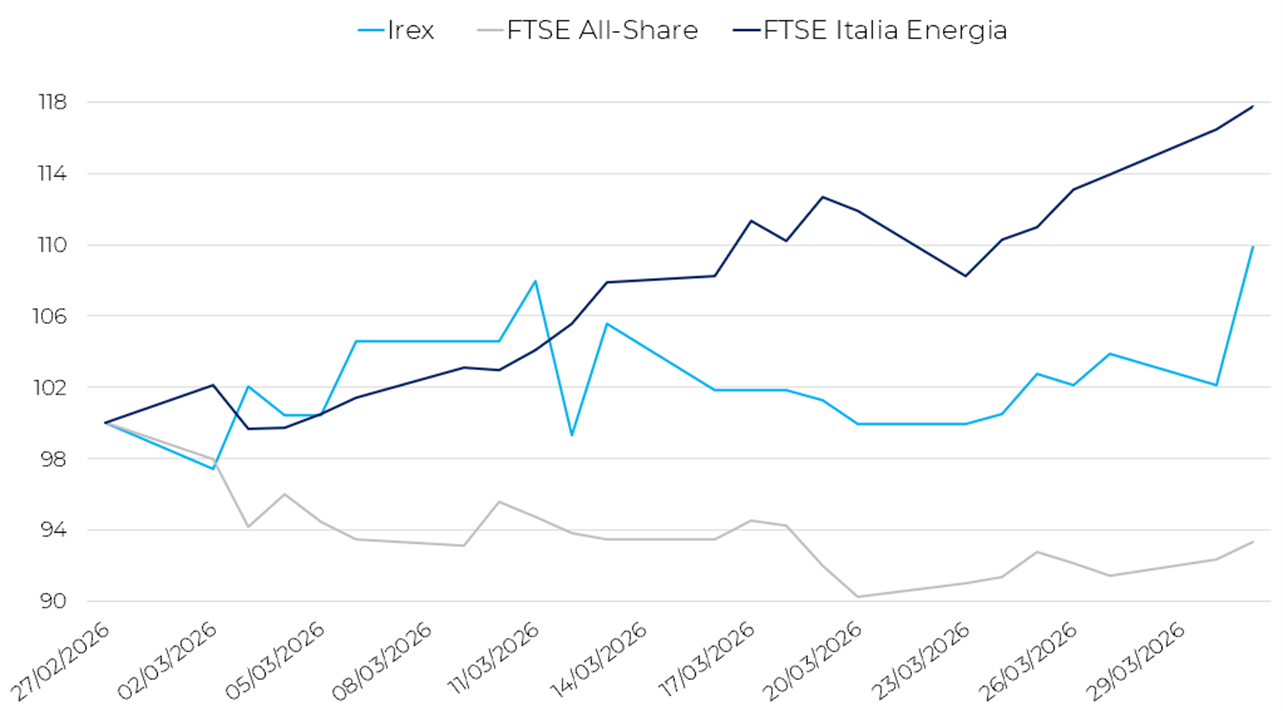

After the rebound recorded in February, the Irex index consolidates its recovery and closes March with a strong gain. The basket of Italian small- and mid-cap companies active in renewables and smart energy stands at 23,520 points, marking an increase of 9.9% compared with the end of February. Monthly performance highlights a particularly uneven pattern. An initial phase of moderate volatility is followed by a sharp mid-month decline, which is quickly absorbed by a strong rebound in the final sessions, bringing the index back to the period’s highs. This volatility reflects an unstable market environment, heavily influenced by external factors and a high sensitivity to macroeconomic and energy-related dynamics.

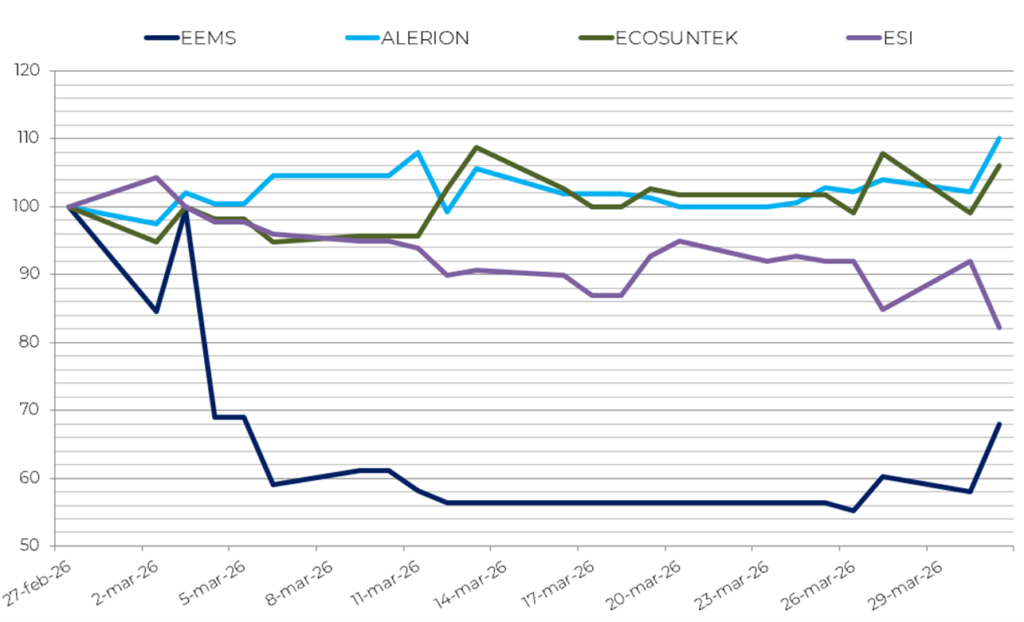

The picture at the individual stock level shows continued high dispersion, consistent with a backdrop of sector rotation and investor selectivity. Among the top performers is Alerion (+10.2%), supported by improving sentiment toward the European wind sector and a greater risk appetite during market recovery phases. Ecosuntek (+6.1%) and Frendy Energy (+4.9%) also post positive results, benefiting from selective buying and greater operating stability. The weakest performances are recorded by ESI (–17.8%) and EEMS (–32.0%), which suffer from a combination of high volatility, low liquidity, and concentrated selling pressure in the lower-capitalization segment.

In the same month, the FTSE Italia All-Share posts a decline of 6.67%, reflecting a deterioration in overall equity market sentiment, while the FTSE Italia Energia records a sharp increase of 17.17%, significantly outperforming the Irex index. This dynamic is mainly attributable to the strong rise in energy commodities, which has supported oil & gas stocks and widened the gap between traditional energy and the renewables sector.

Major European indices also show negative performance in March, amid growing geopolitical uncertainty and financial market volatility. Germany’s DAX posts a decline of 10.15%, while France’s CAC 40 loses 8.97%. Spain is also down, with the IBEX 35 falling by 7.16%. Overall, European markets are affected by a deterioration in confidence, linked to escalating geopolitical tensions and the resulting increase in risk aversion.

On the energy commodities front, March is characterized by a sharp upward shock in oil prices. Brent rises to $118.70/bbl, up 63.54% compared with February, while WTI stands at $101.75/bbl, an increase of 51.01%. In the Italian electricity market, the PUN rises to €143.40/MWh, posting a 25.34% increase month on month.

Overall, these movements signal a significant increase in energy prices. The phenomenon is driven by instability in key production and transit areas, which fuels expectations of scarcity, as well as by speculative strategies. Indeed, the global macroeconomic outlook in March shows a marked deterioration linked to the escalation of the conflict in the Middle East, which has directly affected energy markets and supply chains.

These dynamics are already influencing the macroeconomic environment: global growth is now expected at 2.9% in 2026 (slowing from 3.3% in 2025), while inflation in G20 countries is forecast to rise to 4% in 2026, revised up by 1.2 percentage points compared with previous estimates. In the euro area, growth is expected at 0.8% in 2026, reflecting the direct impact of higher energy prices on economic activity.

Overall, March data confirm that the energy shock represents the main risk factor: rising energy and commodity prices translate into higher costs for businesses and households, with negative effects on demand, inflation, and growth, in a context of heightened geopolitical uncertainty. The development of renewables should therefore be accelerated, both for their greater cost-effectiveness and to enhance energy security.

Worst and best performers