After the weakness recorded in January, the Irex Index opened February with a more favorable trend and ended the period in recovery. The basket of Italian small- and mid-cap companies active in renewables and smart energy stands at 21,405 points, marking an increase of 2.7% compared to the end of January. Monthly performance shows an initial phase of moderate volatility, followed by gradual stabilization and a rebound in the final trading sessions of the month, allowing the index to recover part of the losses accumulated in previous months.

Markets closed before the outbreak of the war in Iran, and the picture at the end of February is not yet affected by the sharp declines in equity markets or by the surge in energy prices.

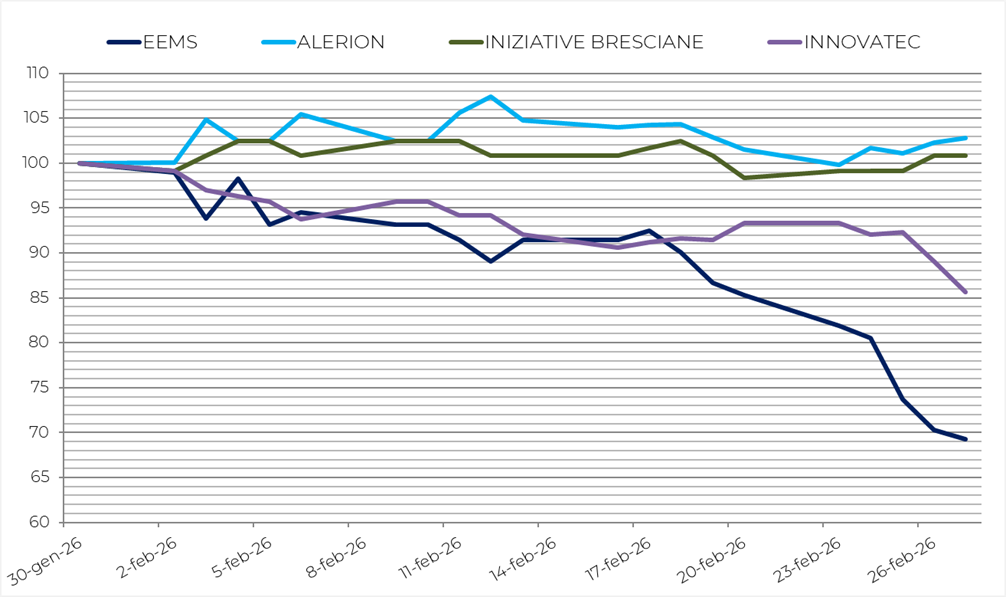

In this still relatively calm environment, individual stocks nevertheless show divergent performances. Among the best performers is Alerion (+2.8%), supported by improving sentiment in the European wind power sector and selective buying interest in the stock. Iniziative Bresciane (+0.8%) also recorded a positive performance, benefiting from greater stability in operating expectations. On the downside, Frendy Energy (–8.0%) and Ecosuntek (–9.4%) posted negative results, while Innovatec (–14.3%) and Eems (–30.7%) were the worst-performing stocks of the month, being more heavily affected by heightened market volatility, which compounded the already weak trend observed in the previous month.

However, Irex underperformed the main Italian equity index. In February, the FTSE Italia All-Share recorded a +15.03% increase, reflecting an overall stable environment for Italian equity markets, while the FTSE Italia Energia rose by +2.24%, closing at a level similar to that of the Irex Index thanks to the contribution of oil & gas stocks.

The main European stock markets also posted positive performances in February. Germany’s DAX rose by 3.15%, while France’s CAC 40 recorded a more pronounced increase of 5.67%. Spanish markets were also positive, with the IBEX 35 up 2.79%, supported in particular by the banking sector and large-cap stocks. Overall, European markets reflect a climate of increased investor confidence, albeit within a macroeconomic context still characterized by elements of uncertainty.

In the energy commodities segment, oil prices continued to rise in February. Brent crude climbed to $72.58/bbl, up 2.66% from January, while WTI settled at $67.38/bbl, an increase of 2.35%. This trend reflects expectations of sustained energy demand and ongoing tensions in the international geopolitical landscape. In the electricity market, the Italian PUN fell to €114.41/MWh, down 13.76% compared to January. The decline reflects more favorable supply conditions and lower pressure from electricity demand relative to the levels seen in the previous month.

Estimates for the international macroeconomic outlook do not yet incorporate recent geopolitical and trade tensions. Global GDP growth is expected to slow to 2.9% in 2026, compared to 3.2% in 2025. Global trade, after growing 4.2% in 2025, is forecast to increase by 2.3% in 2026 (source: OECD). In Italy, the latest available ISTAT data point to a still cautious outlook. In February 2026, inflation, measured by the NIC index excluding tobacco, rose by 0.8% month-on-month and 1.6% year-on-year, down from 1.0% in January. Consumer confidence stood at 97.4, up from 96.8 in the previous month, signaling a slight improvement in household expectations within a still moderate overall context.

The Irex Index therefore reflects a market environment still characterized by high volatility, but shows signs of recovery in February following the declines observed in previous months. While awaiting further regulatory developments and the evolution of the macroeconomic and energy landscape, investor attention remains focused on the financial strength of the companies in the index and on their ability to capture the opportunities offered by the energy transition.

Worst e best performers